Stock

markets. Bull and bear. Trading and investing. Lehman

Brothers (the “Bank

of Evil”). Underneath

these evocative terms and more is a complex, chaotic, non-linear time

series of prices. Their

complexity is such that retail investors may experience feelings of

disorientation with respect to exotic terms like derivatives,

OTC trading, low

latency trading, and dark

pools that seemingly require practitioners to don black robes and

chant around a mysterious circle.

It

is supposed to be straightforward. Select

any accounting and finance text and be treated to chapters on the time

value of money, intrinsic monetary value, cash flow analysis, balance

sheet analysis, income statements, and more to help objectively evaluate

how much an asset is worth now from its likeliness of having some value in

the future. If the investor

calculates the asset is worth buying now at X, then they should buy if it

is on sale for less-than-or-equal to X and pass otherwise. Further treatment on fundamental and technical trading, especially with respect to the Foreign Exchange, can be found

here (updated 2020). Taking it to the other side raises the question of what the

counter-party values the same asset and why.

Adding in third party sell-side analyst reports does the same for

yet another dimension. How

much is the asset worth and who among us is “correct” or has the asset

“mis-priced?”

At

the end of the day, one could apply this technique to buying clothing, or

a car, or a horse and carriage, or anything else at the local department

store or bazaar. Indeed,

markets and derivatives and hidden transactions predate by several

thousands of years the terms “Adjustable

Rate Mortgages, Collateralized Debt Obligations, and Credit Default Swaps”

involved in the latest 2007-2008 economic pain. Only the scale is larger, the layers a little deeper, and the

jargon more heavily specialized. The

result is a long time series that may not be truly random (Lo

& Mackinlay, 1988).

To

help in their analysis, investors have supporting tools such as channel

and trend lines, various indicators, and pattern recognition techniques

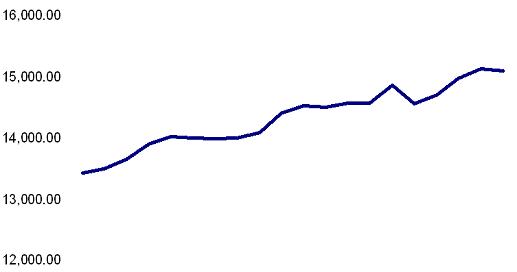

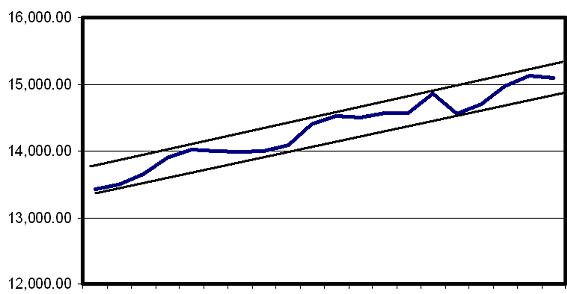

to summarize the time series. These

tools can transform a price time series from this:

to

this:

which

has support and resistance lines, with some uptrending bottom-to-bottom

and top-to-top channel lines that implies the time series – Dow Jones

Industrial Average Q1 2013 – is rising.

These are classic linear tools.

There are also a myriad of non-linear, adaptive tools.

Some of the more famous non-classical non-linear and adaptive tools

are neural networks.

Artificial

neural networks, as applied here as machine learning tools, are in the

broad gray-area intersection between what the brain does and how

(neuroscience) and what a computational algorithm could do (computer

science). Originating as a model of low level neuron anatomy (McCulloch

& Pitts, 1943) and scaling up to a model of self-programming

pattern recognition (Rumelhart,

et al, 1986) artificial neural networks have become a flexible and

powerful tool that greatly extends statistical regression into the layered

depths of non-linear and non-parametric data sets.

Various studies over the past two and a half decades mix variants

of artificial neural networks with financial time series data sets.

Bahrammierzaee

(2010)

compare artificial neural networks on three separate financial services

tasks, including credit evaluation, portfolio management, and financial

prediction. The neural

networks outperformed traditional statistical regression models in all

tasks, especially where the data became highly non-linear.

Rezaiedolatabadi,

et al (2013)

use a hybrid mixture of different artificial neural network techniques to

enhance market prediction on the Tehran Stock Market, outperforming

individual techniques.

Zhang

& Wu (2009)

borrow a technique termed improved bacterial chemotaxis – a variant of a

stochastic, genetic evolutionary algorithm – to blend with an artificial

neural network to enhance its stability, efficiency, and generalization.

These

are very clever and advanced mixture models applied to a complex time

series task. It appears to

make perfect sense – if the market produces stochastic volatility, the

neural network prediction model counters with wavelets and Boltzmann

Machines. It could very well

be that few if anyone on this planet can do better in each of these

particular micro-scale techniques.

But

it must be remembered that artificial neural networks originated as core

models of what the brain does and how.

The intersection with computational algorithms and subsequent

merging into machine learning only arose and lasts with the need for an

objective and testable expression tool.

Artificial neural networks can and do perform complex pattern

recognition. But that only

scratches the surface of what they represent.

Applying neural networks to financial prediction solely because

their advanced non-linear pattern recognition are among the few that fit

chaotic price time series misses the main point.

This would be like an amateur chef stewing a truffle

– it turns a rare, expensive, and complex ingredient into common canned

goods. Truffles happen to be

mushrooms, but a mushroom is not a truffle.

A neural network can do pattern recognition, but pattern

recognition is not a brain model.

This

is especially poignant given that the financial time series dataset is not

a set of data points. Every

tick on a stock price is in reality a buyer agreeing with a seller on the

price. The prices are an

aggregate transaction log, a history of decisions and communications among

the active traders and investors in the marketplace.

These are not simply arbitrary test points on a physical energy

gradient or plane. This is

not the XOR

problem. This is not simply

about covariance matrices and convexity of returns.

These are the beginnings and ends of hopes and dreams for the

future. These spring from the

brain. That taking a

byproduct of a brain model turned neural network and applying it to the

symptoms of human behavior as tracked by financial time series works is a

testament to the dedication and hard work in both fields.

But there is room for something greater.

What

if the core neural network of the brain can directly merge with the cause

of human behavior in a higher-level model?

If human environments in real life are more about interactive

marketplaces than sterile lab data points translated into computational

mathematic algorithms, then perhaps the neural networks of the brain can

merge with financial analysis of human decision making under uncertainty:

Neural networks paired with finance but with cognitive and

neuroscience in the driver’s seat rather than machine learning and

stochastic math. Focusing on

such topics as selective attention,

executive attention, and mirroring neurons, such a partnership would

be behavioral finance on steroids meets executive cognitive development.

Therefore,

fitting artificial neural networks with financial dataset does makes

perfect sense – but very importantly, not simply for the non-linear

machine learning capabilities that are advertised.